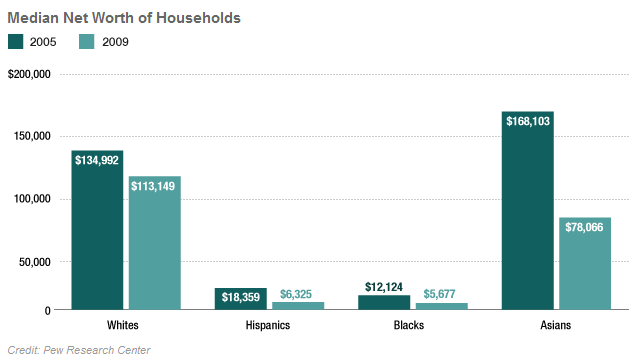

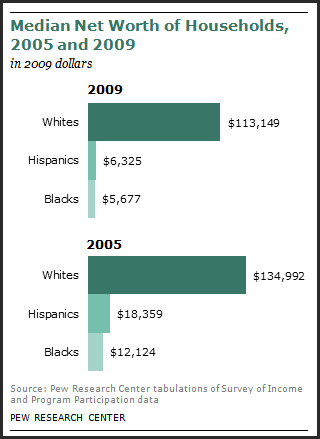

The Great Recession has had a disproportionate impact on the net worth of households depending on their race, according to a new extensive report from the Pew Research Center which analyzes newly-available government data from 2009.

The report summary finds that the housing collapse that began in late 2007 took a far greater toll on the wealth of blacks and Hispanics as opposed to whites. They find, “From 2005 to 2009, inflation-adjusted median wealth fell by 66% among Hispanic households and 53% among black households, compared with just 16% among white households.”

The report summary finds that the housing collapse that began in late 2007 took a far greater toll on the wealth of blacks and Hispanics as opposed to whites. They find, “From 2005 to 2009, inflation-adjusted median wealth fell by 66% among Hispanic households and 53% among black households, compared with just 16% among white households.”

“It’s not so much that the wealthy were busy getting richer – it’s that they slipped back less than those at the other end of the ladder,” says Rakesh Kochhar, a demographer and co-author of the study.

“If you’re less wealthy, you’re more reliant on single assets,” Mr. Kochhar explained. “If you’re more wealthy, you have multiple assets.”

Mr. Kochhar added that because Hispanics and African-Americans are far more likely to be unemployed because of the recession, that has led to a greater decrease in assets. It might mean that blacks and Hispanics have to tap into savings and pension funds sooner than their white counterparts or that they have go into debt to be able to survive.

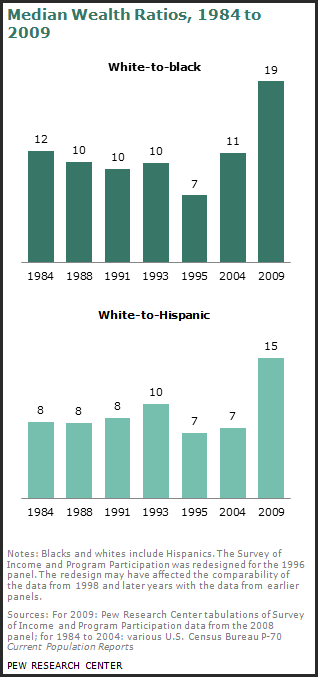

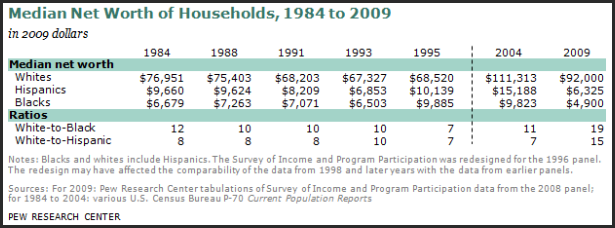

A 25-year look at wealth ratios shows that “the white-to-black and white-to-Hispanic wealth ratios were much higher in 2009 than they had been at any time since 1984.”

The report found that the loss of home values were the principal cause for the decline in household wealth among all groups, but Hispanics in particular were the group hardest hit by the housing collapse.

“From 2005 to 2009, the median level of home equity held by Hispanic homeowners declined by half-from $99,983 to $49,145-while the homeownership rate among Hispanics was also falling, from 51% to 47%,” the report finds.

One explanation is that Hispanics lived in areas that were hit hardest by the collapse. They report, “A geographic analysis suggests the reason: A disproportionate share of Hispanics live in California, Florida, Nevada and Arizona, which were in the vanguard of the housing real estate market bubble of the 1990s and early 2000s but that have since been among the states experiencing the steepest declines in housing values.”

Whites and blacks, however, all saw declines in home equity during this period. They report, “Among white homeowners, the decline was from $115,364 in 2005 to $95,000 in 2009. Among black homeowners, it was from $76,910 in 2005 to $59,000 in 2009. There was little or no change during this period in the homeownership rate for whites and blacks; it fell from 47% to 46% among blacks and was unchanged at 74% among whites.”

Household wealth represents the accumulated sum of all assets which includes houses, cars, savings and checking accounts, stocks and mutual funds, retirement accounts among other assets and is subtracted from debt in the form of mortgages, auto loans, credit card debt among other forms of debt.

This differs from household income, which is the measure of the annual inflow of wages, interest and other forms of earning.

Reports PEW, “Wealth gaps between whites, blacks and Hispanics have always been much greater than income gaps.”

“We know that the income gap is not as large; it has gotten smaller,” said Tatjana Meschede, research director at the Institute on Assets and Social Policy at Brandeis University. “But the wealth gap is stubbornly high.”

Tom Shapiro of Brandeis University, who has studied the racial wealth gap for years, told National Public Radio that he is concerned about the long-term impact of this trend. He believes the wealth gap will likely grow even more, unless the economy turns around soon.

“If a family doesn’t have enough for a safety net for itself, it can’t think about moving forward or moving ahead,” he told NPR.

The researchers also note that while the available two data points, 2005 and 2009, allow for “a before-and-after look at the impact of the Great Recession” they do not line up with the downturn which officially ran from December 2007 and ended in June 2009.

Therefore, in 2005, the housing and stock markets were still rising, leading the PEW researchers to believe that the actual declines are steeper than captured in this study.

They also note, “Moreover, since the official end of the recession in mid-2009, the housing market in the U.S. has remained in a slump while the stock market has recaptured much of the value it lost from 2007 to 2009. Given that a much higher share of whites than blacks or Hispanics own stocks — as well as mutual funds and 401(k) or individual retirement accounts (IRAs) — the stock market rebound since 2009 is likely to have benefited white households more than minority households.”

The critical question is why the housing bubble had a much larger impact on blacks and Hispanics than whites. The answer appears to be that blacks and Hispanics have a much greater percentage of their net worth tied up in housing, as opposed to the stock market and other forms of investment.

Thomas Shapiro, a law and social policy professor who directs the Institute on Assets and Social Policy at Brandeis University, explained to the Christian Science Monitor, “For nonwealthy people in the US, the huge preponderance of the wealth they have is in home equity.”

“As the housing crisis slammed into America,” explains Dr. Shapiro, “it slammed harder” in those states, as well as in low-income communities. Dr. Shapiro also notes that minorities tend to be more recent homeowners, who have had less time to build up home equity.

“White households have been more diversified – they are more likely to own stocks and bonds,” Mr. Kochhar added.

During the period under study, wealth disparities increased, not only between racial and ethnic groups, but they also rose within each group, the researchers report.

They write, “Even though the wealthiest 10% of households within each group suffered a loss in wealth from 2005 to 2009, their share of their group’s overall wealth rose during this period.” From this they conclude, “These trends indicate that those in the top 10% of the wealth ladder were relatively less impacted by the economic downturn than those in the remaining 90%.”

None of this should be very surprising. What is clear is that there remains a pretty substantial gap in terms of net wealth between whites, and blacks and Hispanics.

Despite some gains by the two minority groups since the mid-1980s, the gap is huge and it is growing

Moreover, those minority groups appear more susceptible to economic downturns, and we see the reason why. Most of their wealth is tied up in their homes, whereas whites appear to have a much more diverse portfolio.

The numbers should be frightening however. In 2009, a typical black family had only about $5,600 in wealth; a Hispanic family had about $6,300, while a white family had over $113,000.

Think about that for a moment. Those are just staggering numbers.

—David M. Greenwald reporting

Gives new meaning to the term achievement gap.

It is easier for you to lose half your marbles if you start with only 10 and I have 100 . Is this the Tea Party plan for redistribution of wealth ?(Good Morning Jeff and Rusty)

[i]Is this the Tea Party plan for redistribution of wealth ?[/i]

Good Morning biddlin. I don’t think the Tea Party can ever be accused of attempting a redistribution of wealth. That is the purview of the Democratic Party and Mr. Obama (remember his quote from the campaign “I think we ought to spread the wealth around a little”). Tea Party can more accurately be characterized as wanting to allow those who make the money to keep it, and shrinking the role and size of government.

[quote]The report found that the loss of home values were the principal cause for the decline in household wealth among all groups, but Hispanics in particular were the group hardest hit by the housing collapse.[/quote]

[quote]The report found that the loss of home values were the principal cause for the decline in household wealth among all groups[/quote]

[quote]Whites and blacks, however, all saw declines in home equity during this period. [/quote]

News flash: The gap between the haves and have nots has become wider for ALL GROUPS, whether they are black, white, yellow, red, purple, pink or green. The middle class is disappearing folks! And all that stimulus money didn’t seem to help much, except make the bankers and Wall Street obscenely richer.

That said, during the few years leading up to the Great Recession of 2009 (or whenever the exact year was), redlining was going on. Bank representatives were directed to go into the poorer areas where homeowners were less sophisticated or spoke English as a second language. Bank representatives then sold these naive folks variable rate loans, hiding the messier details of these defective products in fine print, talking a good game to confuse the homeowner. One black woman in particular was sold a variable rate loan she could not afford, to fix her roof, and nearly lost her home – yet she was eligible for a very affordable fixed rate loan. Fortunately legal aid brought suit against the bank and won. She still lives in the house she and her deceased husband lived in for 40 years.

I worked on a case in which someone was talked into converting a non-collateralized loan, which could have been written off in bankruptcy court, to a collateralized variable rate loan on their house. The loan’s rate was written by the month rather than yearly, so it appeared the rate would only be about 1 1/2% (per year would be assumed if you did not look at the fine print and see that it was per month – the 1 1/2% number was about 15 times larger than the print that said “per month” which required a magnifying glass to read). The house was foreclosed on in very short order, when the rates became unmanageable – a house that had been lived in for more than 30 years.

In FLA, robo-courts have been established, to expedite foreclosures, even tho many of the houses do not have proper paperwork in order to even determine if the foreclosure is legitimate. Despite all the ruckus that was raised about banks using robo-signers, that did not check bank paperwork, the practice is still being used w impunity to this day by banks. Nothing much has changed in the banking industry, contrary to popular belief/gov’t propaganda. In fact, if you check your credit card, you will now see it is probably a variable rate interest credit card. Look for a little “v” where it lists interest rates. My card increased from a modest 6% interest rate a few years ago, to about 12% now. The banks snuck this one in…

These issues cross all color lines, and are endemic to the banking/mortgage system as a whole. The current federal administration and Congress have done NOTHING to reform the banking industry and its malicious practices. But then why would they – those gov’t agencies responsible for regulating the banking industry and Wall Street have dept. heads from the very industry it is attempting to regulate. The current head of the SEC defended this practice by saying “but those from the banking and investment industry itself are the only ones who really understand the system”! Egads, could anyone be that stupid/naive? Was she serious? Or just completely duplicitous and caught off guard by the question?

I’ll get off my soap box now 🙂 Argggggggghhhhhhhhhhhhhhhhhhhhh!

Biddlin,

“It is easier for you to lose half your marbles if you start with only 10 and I have 100.”

Maybe if you worked a little harder you could have 100 marbles too instead of relying on the Gov’t to take someone else’s marbles and give them to you.

I would think our local leftists would think of this as excellent news.

THe wealth difference between whites and blacks, according to your chart, has fallen from:

2005

$134,992 -$12,124 or a wealth gap of $122,880

2009

$113,149 -$5,677 or a wealth gap of $107,472

The wealth gap has decreased by over fifteen thousand dollars.

Surely this is something to celebrate among those who want equal outcomes.

Now it’s true that the gap has closed because everyone is poorer. But more equality, not more wealth, is the goal of Democratic party economics, when stripped to its essence.

As an interesting thought experiment, suppose the figures had gone the other way, with 2005 and 2009 interchanged. Is there any chance this article would have been written with the same slant, decrying the increase in the wealth gap between racial groups?

Hey rusty, I think I’ve worked pretty hard the last 45 years . I’m in that group that was stupid enough to get old and disabled only to discover that Snoopy had buried all the premiums I had paid for 25 years and wouldn’t dig them up and my deferred comp fund manager was most apologetic that he lost 70% of my money, but the other thirty would almost certainly cover his expenses., but I’m not bitter about it ! Elaine is right . This recession has cut everybody who works for wages, and the small businesses that they support, deeply ! In 2001 I was assured by my insurance agent and accountant that my wife and I were in fine shape . A chronic illness and a career ending injury combined with the loss of our retirement savings in the comp account and Met Life’s denial of benefits pretty much wiped us out financially ! Good thing I like playing music on the road !I know you folks in Davis are sensitive about being perceived as racists . I don’t think that is what this is about . It is factual that until the middle 1960s, white males had a huge legal and economic advantage over other groups in this country ! That head-start resulted in a disparity of wealth that was diminishing and now is growing again at a rate that is alarming .

“I know you folks in Davis are sensitive about being perceived as racists.”

Oh really. I think anyone is sensitive about that no matter where they live.

I’m concerned about the tone of the early comments here. David has summarized a report by which we should be traumatized, the dramatically uneven suffering brought on by this recession. Individual cases of misfortune tell part of the terrible story. Numbers like these, however, remind us of systemic problems we need to solve. And, yes, it’s ALL about race.

Worst of all, the gains by Tea Party types combine with the financial interests of very richest Americans to leave us ill-equipped to make any progress in reversing this unhealthy racial and economic divide. Talk about loosing one’s marbles!

Rusty49

What if my 100 marbles came to me as an inheritance from my slave owning great grandparents and I have never worked a day in my life. Still ok with that distribution ?

Wow medwoman, that is quite a post. Given that a very small percentage of folks descended from slave owners or inherited any wealth, and even fewer have “never worked a day in their life”, the post provides little substance. Very different from your normal posts, which are usually substantive, even if I tend to disagree with your viewpoint.

Provided that wealth has been accumulated in a lawful manner, I just don’t see any justification for taking away money from folks who have it and giving it to folks who don’t.

Ia agree that the disparity in wealth is not healthy for the country or the world, but taking it away from one group to give to another isn’t going to help solve the problem.

“What if my 100 marbles came to me as an inheritance from my slave owning great grandparents and I have never worked a day in my life. Still ok with that distribution ?”

Medwoman, anyone can come up with any scenario they want to try and build up their position. I’ve got one for you:

What if someone had a good paying job but bought a house they really couldn’t afford, 2 new BMW’s, a boat, furnished that house to the hilt, took lavish vacations and gambled and spent until they went broke would they still be entitled to some of my hard earned and wisely saved marbles?

ERM–good news flash! I wanted to present some of your points, but you did it better than I could have.

It would be interesting to see what those stats look like if you left out the top 5% in each racial group.

I suspect you would see much less disparity between the racial groups for the bottom 95%.

The real shift in wealth is that those who already had wealth (mainly some whites) did not lose much of it; whereas those who didn’t have many assets (all colors, including most whites) lost a substantial portion of what they had.

Rusty, I know you hate hypothetical questions, but if you were working in a coal mine and the canary died, would you blame the bird or get out of the mine ? The fact that the less established, less educated and poorer people of our country are being choked by poverty should be a warning to us all !